The Problem:

Most nano businesses – the corner tea shops, street food carts, istri wallas, fruits and vegetables hawkers, hole in the wall tailors, tiny provision stores, etc – are informal in nature. Less than 10% of the businesses we work with, have any form of documentation which formalizes their existence. Majority of their earnings are in cash and hence non-verifiable. Hence lending to these businesses comes with its own set of challenges, which at present are overcome only by the informal, local money lenders. Over 500 such nano-entrepreneurs participated in our Udhyami programme (to be discussed in detail later). 100% of the cohort was banking enabled, yet more than 75% of them reported that they depended on informal lenders and/or personal savings for their credit needs.

Typical credit needs for the nano-entrepreneurs are in the range of INR 5,000-50,000. In business, credit is most commonly accessed for replenishing inventory. Medical emergencies, children’s education fees, major festivals/family events are the other most common reasons for accessing credit. In rare cases credit is needed for investment into equipment and/or infrastructure and the size of credit required ranges from INR 10,000 – 1 lakh.

Major reasons for depending on informal sources of credit

- Easier to access, small ticket size loans (5-25k) from informal sources.

- Option to repay loan on a daily or weekly basis (hence smaller due amounts) from the convenience of their homes/shops

- Credit needs are poorly anticipated and often urgent, with capital being required within a day or two. Informal lenders are far more easily accessible under such circumstances than are formal lending services.

The lack of options for formal sources of credit for this audience is because of the difficulties in underwriting such loans and the disproportionately high cost of operations anticipated, in order to service such small loan amounts. Moreover as mentioned in point #2 above, this audience is more familiar and comfortable with daily or weekly repayment of loans as opposed to a monthly schedule. Hence replicating this model of daily/weekly repayments would make it easier for them to shift to formal credit products than to expect them to adapt to a monthly payment plan. However such a model would further increase the cost of operations.

The poor anticipation of credit needs primarily results from the lack of tracking of income and expenditures, and due to irregular savings behaviour prevalent across this audience. Solving this problem requires greater efforts beyond solving for access to credit alone and more towards other services such as financial planning, savings, insurance etc., adaptively designed for this audience

There have been a number of smartphone-app-based instant loan providers in recent times. Such apps do cater to urgently required small ticket size loans. However, the underwriting of such loans are done via algorithms requiring an extensive set of data points, which is difficult to collect (verifiable income, as stated earlier, is one example of such a data point that is often unavailable) from the nano-entrepreneur segment. Such apps are also not very user-friendly, and are rarely designed keeping this audience in mind, which in turn leads to reduced repayment rates, thereby requiring frequent follow ups via phone calls or in-person visits to keep repayments on track.

The Udhyami Program:

The Udhyami program was started by Udhyam Vyapaar in the immediate aftermath of the first wave of covid induced lockdowns in 2020. The goal of the programme was to enable nano-businesses to restart and restore their income, following an unprecedented, months-long shutdown period. The support provided to enable such a restoration was a combination of access to interest-free micro credit, business plan ideation, and formalisation and digitization assistance.

The cohort comprised a total of 556 (260 female and 296 male) nano entrepreneurs, in and around Bengaluru. This audience of nano businesses comprised street food stalls, tea shops and bakeries, ironing and laundry services, home-based resellers, small clothing and tailoring shops and kiranas.

The credit support was provided as a returnable grant of INR 5,000 – 10,000 per entrepreneur. The entrepreneurs upon successfully investing the grant amount and restarting their income flow, were morally obligated to return the grant amount. This recovered sum was then disbursed again as a returnable grant to another cohort of similar entrepreneurs. The capital for the grants was fundraised partly from a CSR fund and partly via crowdfunding.

The returnable grants provided us an opportunity to experiment with, observe and learn about credit repayment behaviours of these nano-entrepreneurs. As stated in points 1 & 2 above, their reasons for dependence on informal credit were multiple. We understood that these entrepreneurs are comfortable with informal loan products because they offer a daily repayment schedule. Hence we designed the terms of the returnable grant to mimic a typical loan from their local money lender. Such a lender would lend an amount of INR 9,000, which then would be repaid by the entrepreneur as daily instalments of INR 100 over a period of 100 days (total repayment of INR 10,000 for an INR 9,000 loan). The Udhyami grants (interest-free given they were grants, didn’t require any interest payment) were likewise designed with the option to repay daily instalments of INR 100 for a period of 50 days or 100 days for grant amounts of INR 5,000 and INR 10,000 respectively.

The option of daily repayments however introduced another problem. Collecting, reconciling, monitoring and following up for daily repayments from a cohort of 500 entrepreneurs spread across the city, meant either investing heavily in operations or innovating.

QR code enabled recollections:

We partnered with two fintech startups – Supermoney and Buildd – for the disbursement and recollections of the returnable grants. Given neither the fintechs nor ourselves had enough feet on ground to be servicing 500+ loans that had a daily repayment structure, we tried to enable digital repayment of loans. To do so, insights from one of Udhyam Vyapaar’s earlier initiatives provided a starting point.

Prior to the pandemic, we had had a brief experience with enabling digital repayments via QR codes as part of our Istri Project. We had created access to finance for the purchase of LPG-fueled istri boxes via another fintech startup, Gromor. We quickly learnt that fortnightly repayment cycles would lead to greater repayment rates compared to monthly cycles, as the amount to be repaid during each cycle was smaller and hence more easily saved and dispensed with. However the next few weeks saw us struggling to recollect loan payments, necessitating that we had our field staff spend majority of their time visiting the 110+ shops spread across Bengaluru on a very frequent basis, thanks to irregular repayment at the time of the pre-scheduled visits.

Hence we wanted to experiment with ways to digitally recollect the loans. We decided to collect payments via UPI as most vendors already had a UPI ID linked with their bank accounts. The problem however was that more than 50% of the vendors used UPI only to receive payments and didn’t know how to make a payment. However, they had all seen their customers make payments by scanning QR codes posted on their shop fronts. So we created a QR code and stuck it in our borrowers’ shops/carts and asked them to scan the code to make the payment.

The QR code mode of repayment, coupled with the fortnightly repayment schedule, significantly increased the rate of repayment, while simultaneously reducing the number of shop visits. Repayment rates shot up from less than 70% to more than 90% in the subsequent weeks and stayed there until the pandemic hit. However there still was one major problem. We noticed that the vendors frequently used multiple UPI accounts (belonging to their friends and family members) to make payments and hence reconciling the payments was impossible without further phone calls or field visits.

Learnings from the Istri Project lending experience were incorporated into designing the repayment model for the Udhyami programme. Having decided to provide the option of daily repayment of loans we adopted the QR code based repayment method. But in order to avoid the reconciliation issue faced earlier, we decided to provide each borrower with a unique QR code, linked at the backend to a unique customer ID. The unique ID would enable us to map all repayments made by scanning the QR to the right customer, regardless of the UPI account from which the payment was made. Over time we learnt that the vendors had learnt to scan their respective QR codes from the photo gallery on their smartphones, and hence there was no need to give them a printed version of the QR code even.

Sample of the unique QR code

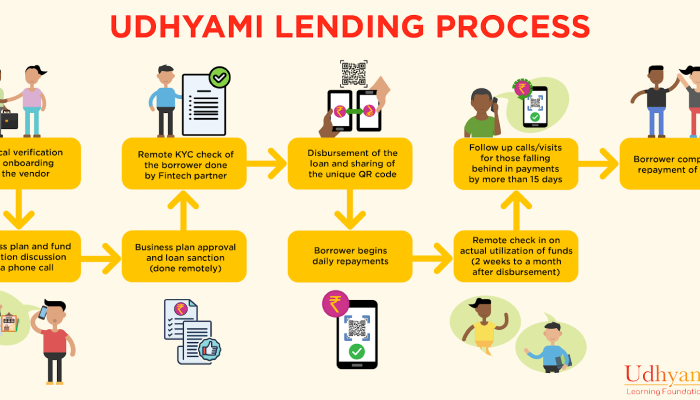

The Process:

Stakeholders & Their Experience :

“Repayment of the Udhyami loan has been very easy. As all payments are made via UPI, there is no need to visit a bank and no problems such as missing a payment due to check bouncing. I have started requesting my customers at my shop to pay me via UPI so that I will have enough money in my account for the daily payments.”

– Kantha HN, Street Food Vendor (Udhyami Borrower)

“Repaying via UPI, a daily amount of just 100 rupees means that I can independently repay this loan from my income without anyone’s support. Each repayment takes only about 5-10 seconds and I do it from the convenience of my shop.”

– Radha, Self-Employed Tailor (Udhyami Borrower)

Working with Udhyam on the program has been a learning experience for Supermoney as well. A key difference in creating the repayments solution for the beneficiaries was that we needed to ensure the solution was simple to understand and easy to implement for all stakeholders. Mapping a unique dynamic QR code for payments through UPI for each beneficiary achieved multiple objectives of giving a simple scan and pay option for customers while simplifying the reconciliations at our end. Typically repayment solutions are a standard suite of card based, netbanking or debit to bank account options. However the nature of the cohort needed an innovative solution that is now extended across cohorts by us.

As a result of this program, we notice beneficiaries are able to easily make repayments every day and repayments becoming a daily habit as against being a push effort. To build further on this would be to map the repayments to a hybrid credit score for the beneficiaries so that they can integrate into the formal financial ecosystem.

– Nikhil Banerjee, Founder and CEO, Supermoney (Fintech partner for the Udhyami project)

“We at buildd are creating the future of API banking, our team has two decades of experience in lending products & financial technology. For Udhyami we deployed a unique QR based integrated repayment mechanism on top of our CRM tool which works on a rule based engine to assign UPI QR per customer creditline & captures repayment in real time for updation. Also the CRM keeps the customer updated on his due date & due amount well before in time. The system is more to do with educating the customer with the facility that he has been provided & his benefit of paying on time, rather than a collection tool. Also a complete whatsapp user onboarding flow, loan management & repayment journey has been developed by Buildd for Udhyami customers, they find it easy to communicate on whatsapp chat in their language and this could enable varied credit use cases via the whatsapp platform

Udhyami portfolio cohort has been consistently performing with on time collections being 75% & rest being collected within a week without any physical call or visit, this is unprecedented in the industry. The local language messaging too has helped achieve these numbers.”

– Sachin Gaikwad, Founder and CEO, Buildd.in (Fintech partner for the Udhyami project)

Repayments :

On-time repayment rates stayed at 70-80% through the entire duration of the programme, and this was possible with a field staff to vendor ratio of 1:80 and each member of the field staff having to spend just under a week per month on field visits.

Repayment behaviour was also aided by a simple social nudge. We set up a WhatsApp group with all the borrowers. These groups were the only consistent reminders for repayment. As the entrepreneur paid his/her daily repayment amount, he/she was requested to share the update on the group, which in turn served as a nudge to the other members of the group to remit their dues as well.

The WhatsApp group was an attempt to virtually simulate the group meetings in the JLG(joint liability group) model.

Udhyami recollection stats:

1st cohort of 253 nano entrepreneurs

This cohort received the loan amount just prior to the second wave and the ensuing lockdown in April 2021.

- Repayment rate prior to 2nd lockdown – 80%

- Repayment rate during the 2nd lockdown period – 50%

- Total recollections as on date (following the resumption of repayments after businesses reopened in July 2021) – 70%

It is important to note that Udhyam Vyapaar’s focus while shortlisting recipients for the returnable grants was on lending to those in dire need of capital to restart their livelihoods and not on minimizing risk of lending. Our follow ups for repayments were often gentle virtual nudges rather than resource intensive field follow ups. Just about 20-30% (on average) of the borrowers required follow ups via phone calls and/or field visits throughout the period of loans.

2nd cohort of 303 nano entrepreneurs

This cohort received the loan between Dec2021 & Jan 2022.

- Repayment rate as on date – 80%

- Expected recollections by close of program – 90%

Additionally, our data reveals that only 25-30% of the total cohort of borrowers required follow-ups for repayment.

Through the entire tenure of the loan, the 70% who repay in a timely manner require just a single field visit – at the time of verification of business prior to disbursement.

The remaining 30% entrepreneurs require on average 2 phone calls per month and 3 field visits during the entire loan tenure.

Overall, we have found via this project that a unique QR code based loan recollection tool can significantly bring down the operational cost typically expected for a product that entails a small loan amount and a daily repayment frequency.

This opens up the possibility for future lending to this audience segment, and an opportunity to anchor them more firmly in the formal financial ecosystem.